In its most recent review, the Institute for Fiscal Studies (IFS) revealed that 9 out of 10 middle-earning private sector workers do not save the recommended 15% of their salary for retirement. Which part of that grouping do you fall into, how much does it matter, and what practical steps can you take towards retirement planning instead of harbouring the worry?

If you’re one of the minority that save the proportion of your salary that the IFS recommend, take a minute to congratulate yourself. This article is useful for you too, because planning is as much about setting your retirement intentions and goals and understanding the best strategies and investment approaches to achieve them as it is about making sure you’re putting enough money into your pension.

If you’re among the majority of people that do not save 15% of your salary, this article should help you understand why preparation for retirement is so important, what might happen if you forgo adequate planning, and some of the tax-efficient options available alongside traditional pensions that may prove useful for developing growth.

Planning for retirement - what do you need to consider?

Where should you start with planning? A good place to begin is by establishing what you hope to get out of your retirement. Naturally, there are elements of our retirement that are within our control, and elements that are not. We’ll start with those things within our control that you should be considering:

- When do I want to retire?

- What do I want my retirement to look like?

- How much should I contribute to my pension?

- Am I taking enough risk to achieve my retirement goals?

- What can I do today to make my retirement vision a reality?

It may seem counter-intuitive, but high-earners will find they have an even more challenging task than others. They are likely to have the most ambitious retirement goals but suffer most from limitations on pension allowances, the recent reduction in the capital gains tax free allowance (which fell from £12,400 to £6,000 in 2023, and will fall again to £3,000 in 2024) and have additional concerns around the taper on allowances that can limit or entirely remove the tax benefits of saving into a pension if certain income thresholds are surpassed.

Going beyond the basic pension and considering risk

The mistake many people make when planning for retirement – in addition to not putting enough money aside for retirement – is to consider their pension allowance the sole vehicle to rely on. Advisers are becoming increasingly aware of the impact of underfunded pensions and the impact of tapered pension allowances on high earners, and are turning to tax efficient investments to meet their clients’ needs.

High earners

For high earners at risk of tapering pension allowances, the need for additional options is perhaps most pressing. Believe it or not, it is not always simple to avoid falling into the tapered annual allowance once you factor in pensions savings and employer contributions, and calculating your adjusted and threshold income to insure you are not subject to the taper is a complicated process that most people should entrust to a financial adviser. You can read more about how it works on gov.uk.

This group in particular turn to their financial advisers to find out more about what their options are for pension saving that won't see their annual pension allowance tapered, because their options around their primary pension are limited. This group is also in a position to put a larger amount of money at risk.

The rest of us

Those with more intermediate salaries should also consider additional tax efficient investment options beyond a traditional pension scheme or SIPP simply for the combination of tax reliefs and the potential for high returns that these schemes can offer. Naturally, for this group, there is a decision to be made about whether to simply increase pension contributions, or whether to make a higher risk investment with what would amount to at least one year's worth of personal pension contributions or more.

Investment schemes like SEIS and EIS offer tax reliefs that are extremely complimentary to traditional pension schemes, offering guaranteed tax reliefs around income tax, capital gains tax, and exemption from inheritance tax. What’s more, for a relatively small initial investment (in some cases, just £5,000) they can diversify existing portfolios and open investors to the potential for very significant growth. Most EIS funds, for example, target returns of 3x, but if your portfolio contains the next Uber or Deliveroo, it could be many times this.

Pension saving is a long-term process by its very nature, so the fact that tax efficient investment schemes like SEIS and EIS are long term, illiquid investments is less of a drawback than it would otherwise be. Venture capital trusts (VCTs) are slightly different, as they can they pay out regular dividends. But, with VCTs the returns can be muted as you are buying into an existing portfolio of companies and potentially paying for growth that has already happened.

The right amount of risk

Investing in tax efficient schemes outside of traditional pensions is often about being open to increasing the risk profile of an investment portfolio in exchange for higher growth. How much risk are you adding, how much is too much, and how much is right for you?

Research by Hardman & Co. found that investors with normal risk profiles (equity:bond portfolios that are between 60:40 and 80:20), who add an appropriate proportion of venture capital (10-20%) can add 0.5-1% to expected annual returns without increasing overall portfolio risk, even without any tax reliefs. Long term, these small percentages add up.

Even if you decide to make tax efficient investments like EIS or SEIS a larger proportion of your portfolio, a quick calculation can bring into focus what you stand to gain vs what you stand to lose.

One option: EIS investing alongside pension contributions

The average annual pension contribution, based on a salary of £32k, is £2,060.80. For the last 40 years, UK pensions have averaged around 7% growth.

As demonstrated in our recent UK startup index, the UK startup market grows by an average of 25%-31% annually. Comparing this to the 7% growth average of pension funds would be misleading because you can’t invest in the entire UK startup market, but it gives you a sense of the potential growth available when things go well for EIS investors, as well as the value accrual taking place in the UK startup market.

For a one-off investment of £10,000 in an EIS fund, which takes around seven years to mature (though it can take longer), you are able to make significant tax savings and potentially see greater growth than you would for paying the average pension contribution into your pension annually for seven years.

Assuming we are taking a calculated risk and investing £10,000 in EIS, what does this actually get us, and what do the outcome scenarios look like?

1. What you get for a £10,000 investment providing conditions are met. The examples below assume the investor is a higher rate taxpayer:

30% of your investment as income tax relief: £3,000 back from HMRC (less fees).

The option to defer any capital gains for as long as you hold EIS shares. Let’s assume you defer a capital gain of £5,000 realised on the sale of a second home two years previously, and on which you’ve already paid capital gains tax at 28%. You can request HMRC return the £1,400 you paid in capital gains tax, and you won’t need to pay this until you sell your EIS shares. Even if you sell your shares, you can invest another £5,000 in EIS (an amount equal to the gain) and defer the gain again if you choose.

No capital gains payable on disposal of your EIS shares.

Your EIS shares qualify for Business Relief (BR). Provided you hold them for two years at the date of death, they will qualify for 100% IHT relief.

If your shares fall below their original value (less any income tax relief claimed), you can claim loss relief which can be offset against income tax or capital gains tax.

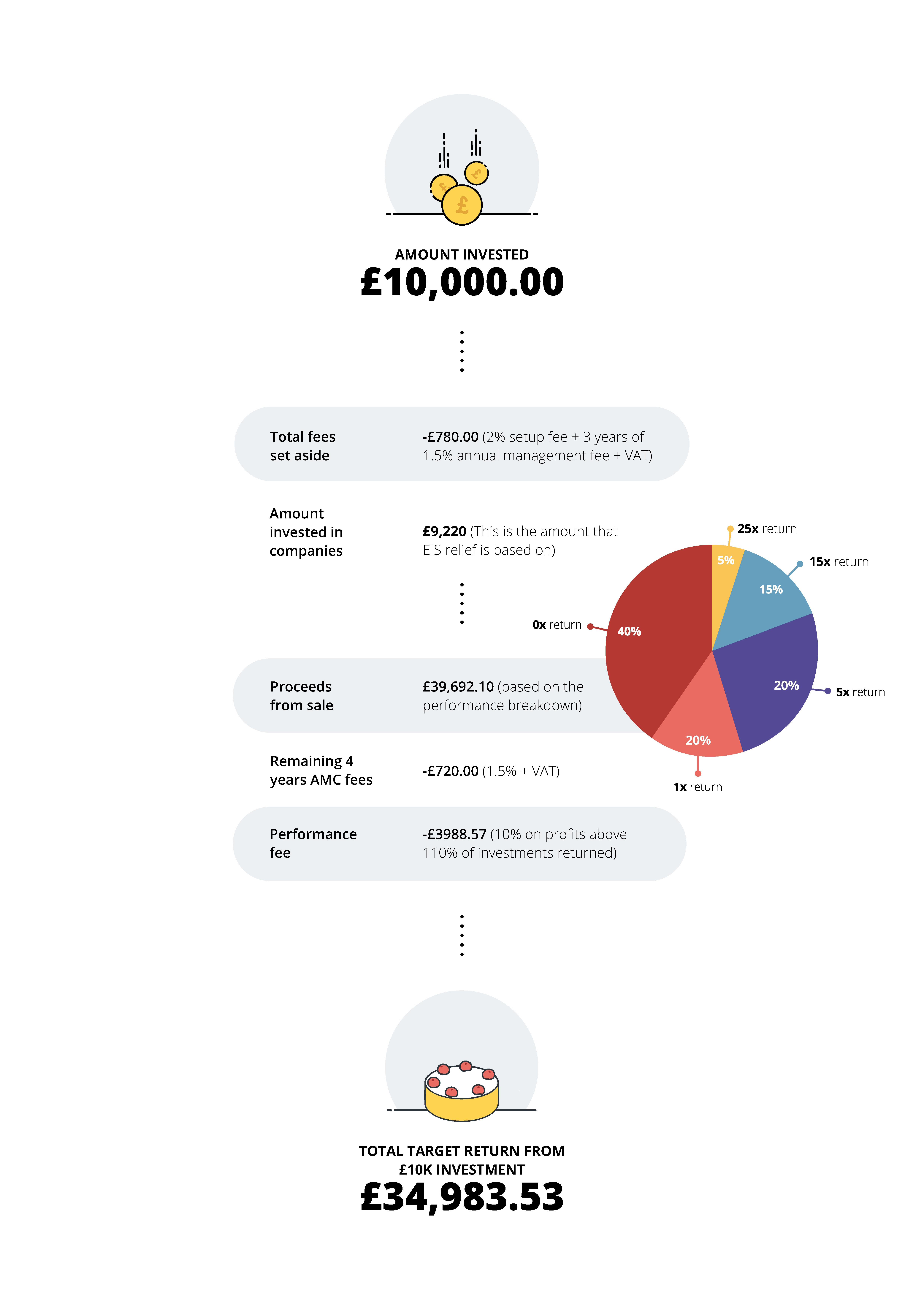

2. What you have the potential to receive - positive scenario.

In addition to the tax relief you’ve already received, if you follow the data-principles of the Access EIS Fund and invest in a large portfolio – around 50 companies – you now hold shares in 50 companies in a fund targeting at least 3x growth.

This is what that looks like in a positive scenario, if 10k is invested.

Risk is not for everyone

It goes without saying that begininning to look into higher risk, higher growth strategies alongside traditional pension saving won't be an approach suitable for everyone. There are a wide range of approaches to managing your pension and the best option for each individual will vary with their individual circumstances. We encourage everyone to seek advice from a financial adviser before making any decisions or investments.

The Access EIS Fund

Our fund co-invests with proven angel investors to build large portfolios of hand-picked companies for our investors. It’s a high risk investment, and we can’t guarantee that every startup will be a unicorn, but we’re confident that our approach is the smartest on the market. Even better, we can show you the data to prove it.

To find out more about how the Access EIS Fund can work for you or your clients. Use the link below to schedule a call with one of our product experts.

What is Access EIS?

Read our fund brochure for everything you need to know about the Access EIS Fund, from the specifics of our innovative co-investment model to our fees, and how to invest.

Register to learn

more about our data,

fund and venture capital