Don't invest unless you're prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong.

Updated: January 2026 | By: Tom Britton, Co-founder

With the significant reduction in capital gains tax (CGT) and dividend allowances over the last two years, protecting your returns has never been more critical. For high-net-worth individuals and sophisticated investors, "tax-efficient" no longer just means an ISA. It means building a diversified portfolio that utilises the UK’s world-leading venture capital schemes.

In this guide, we break down the seven most effective tax-efficient vehicles for 2026, from core staples to high-growth alternatives.

Investment type | Income tax relief | CGT treatment | Max annual investment |

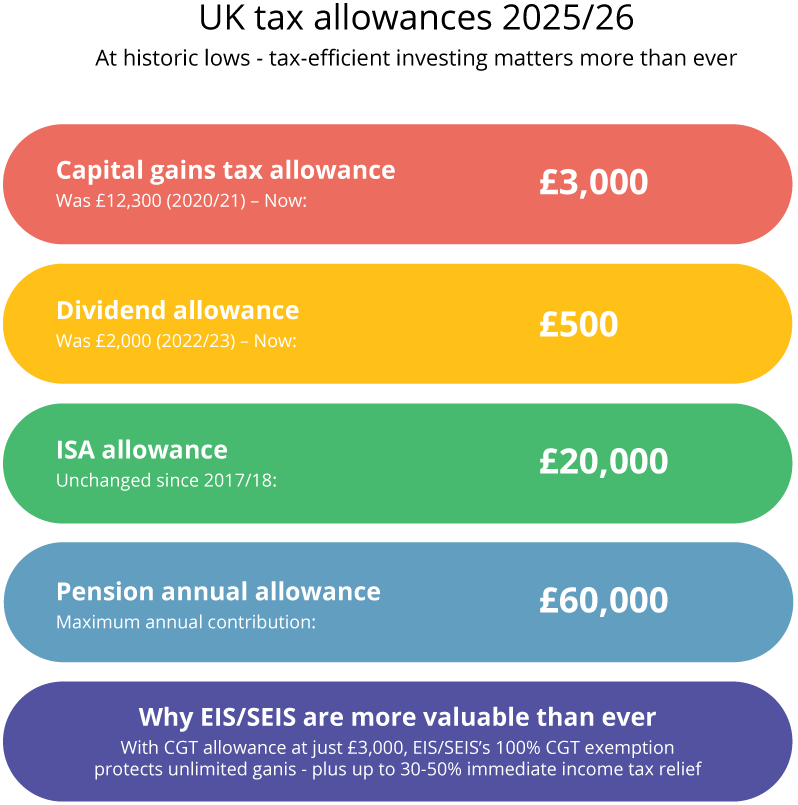

Pensions | 20% – 45% | Tax-free growth | £60,000 (Annual allowance) |

Stocks & shares ISA | N/A | Tax-free growth | £20,000 |

SEIS | 50% | Tax-free growth / 50 % 50% reinvestment relief | £200,000 |

EIS | 30% | Tax-free growth / Deferral relief | £1m (£2m for KIC) |

VCT | 30% (20% from April 2026) | Tax-free dividends & growth | £200,000 |

AIM shares | N/A | Tax-free (if in ISA) | £20,000 (ISA limit) |

Gilts | N/A | Exempt from CGT | No limit |

The most significant tax-planning tool for most UK taxpayers. Contributions are made "gross," meaning a £10,000 investment only costs a higher-rate taxpayer £6,000.

Best for: Long-term retirement planning and mitigating 40%/45% income tax bands.

The 2026 view: With the lifetime allowance removed, pensions have become an even more powerful tool for high earners to shield large sums from HMRC.

The "bedrock" of any portfolio. While you don't get upfront tax relief, every penny of growth and every dividend payment is shielded from the taxman forever.

Strategic tip: With the dividend allowance now at its lowest historical levels (£500), moving dividend-yielding stocks into an ISA is a priority for 2026.

Flexibility: Unlike pensions, ISAs allow you to withdraw your capital and any tax-free returns at any time, making them an essential tool for medium-term goals or as a tax-efficient emergency fund.

For those with a higher risk appetite, SEIS offers the most generous tax breaks in the UK.

An incomparable tax relief: An investment of £10,000 effectively costs just £5,000 after up to 50% initial tax relief (subject to individual circumstances). If you utilise CGT reinvestment relief, that net cost can drop even further, though all capital remains at risk and may be lost entirely.

Startups to unicorns: Our research shows SEIS is often the entry point for the "unicorns" of tomorrow, though it requires a minimum three-year holding period to retain reliefs.

Inheritance tax relief: SEIS shares qualify for inheritance tax relief by qualifying for Business Relief.

Worked example A

Investment: £10,000

Income tax relief (up to 50%): £5,000

Effective net cost: £5,000

Scenario 1: Investment succeeds (3x return)

Exit value: £30,000

Gross gain: £20,000

CGT saved (up to 24% higher rate): £4,800

Total value after tax benefits: £34,800

Scenario 2: Investment fails completely

Loss for tax purposes: £5,000

Loss relief at 45%: £2,250

Effective final loss: £2,750

Some funds combine the tax relief and potential returns with an impact focus. Carbon13's SEIS fund focuses on high-impact, climate-tech ventures. Explore the Carbon13 SEIS fund page to see how we apply this relief to the green economy.

The "big brother" to SEIS, designed for slightly more mature startups.

The math: At a 30% relief rate, a £100,000 investment has a net cost of £70,000.

Loss relief: One of the most overlooked benefits. If an EIS company fails, you can offset the loss against your income tax. For a 45% taxpayer, this means total "at-risk" capital is significantly reduced (down to roughly 38.5p for every £1 invested).

Inheritance tax relief: EIS shares qualify for inheritance tax relief by qualifying for Business Relief.

Worked example B

Investment: £100,000

Income tax relief (up to 30%): £30,000

Effective net cost: £70,000

Scenario 1: Investment succeeds (3x return)

Exit value: £300,000

Gross gain: £200,000

CGT saved (up to 24% higher rate): £48,000

Total value after tax benefits: £348,000

Scenario 2: Investment fails completely

Loss for tax purposes: £70,000

Loss relief at 45%: £31,500

Effective final loss: £38,500

*Choosing between SEIS and EIS often depends on your specific tax year goals. For a deeper dive, listen to our Angel Insights podcast with Aled Phillips from Niche Private Clients as he weighs the risk-reward profiles of both schemes. Both SEIS and EIS allow you to carry tax relief back one tax year.

VCTs offer a way to access a diversified portfolio of early-stage companies via a London Stock Exchange-listed vehicle.

Why investors love them: Tax-free dividends. In a landscape where dividend tax-free allowances have been slashed, VCTs remain one of the last "pure" ways to generate tax-free income.

Timing: VCT "season" typically peaks between January and April. Note: Following Budget 2025, the rate of income tax relief for VCTs will reduce to 20% from 6 April 2026 (down from 30% in the current 2025/26 tax year).

Investing in the Alternative Investment Market (AIM) has traditionally been valued for its inheritance tax (IHT) benefits through Business Property Relief (BPR), though significant changes from April 2026 will substantially reduce this advantage.

Current rules (until 5 April 2026)

Many AIM-listed companies qualify for up to 100% Business Property Relief

- After two years of ownership, qualifying shares can be passed on inheritance-tax-free

- Potential to save up to 40% on estate value above the nil-rate band

Major changes from 6 April 2026

From 6 April 2026, AIM shares will only qualify for 50% Business Property Relief (not 100%).

This means:

- Effective IHT rate: 20% (vs 40% standard rate, or 0% under current rules)

- Example: £1m in qualifying AIM shares = £200,000 IHT after April 2026 (vs £0 currently)

- This applies to ALL AIM holdings regardless of value

- There is no transitional protection for shares purchased before April 2026

In a higher-interest-rate environment, gilts have made a comeback.

The loophole: While the "coupon" (interest) is taxable, the capital gain on gilts is CGT-exempt. For investors buying "low-coupon" gilts at a discount, this provides a highly predictable, tax-efficient return.

Strategic allocation: Gilts can be held outside of an ISA without incurring capital gains tax on the profit made at maturity. This makes them an excellent secondary option for those who have already maximised their £20,000 annual ISA allowance.

As Syndicateroom CEO Graham Schwikkard highlighted in his research paper covering the power law:

"In the current market, tax efficiency is only half the battle. With the majority of investment returns generated by a tiny fraction of investments, investors should aim to diversify their portfolios in a data-driven way."

For those looking to include SEIS and EIS investments in their portfolios, our analysis of tax-efficient investing in a digital world suggests that investors who diversify across at least 30+ startups are statistically more likely to see positive net returns than those picking individual "winners".

Yes. Schemes like EIS, SEIS, and VCTs involve investing in small, unquoted companies. Their value can go down as well as up. The tax reliefs are designed by the government specifically to compensate for this higher risk.

What is the 2025/26 capital gains allowance?

For the 2025/26 tax year, the individual tax-free allowance (Annual Exempt Amount) for capital gains is £3,000. Gains above this amount are generally taxed at 18% (basic rate) or 24% (higher rate) for shares. Utilising the 100% CGT exemption offered by EIS and SEIS remains one of the most effective ways to protect your upside.

What is the 2025/26 dividend allowance?

The tax-free dividend allowance for the current tax year is £500. Dividends exceeding this amount are taxed based on your income band: 8.75% for basic rate, 33.75% for higher rate, and 39.35% for additional rate.

How do I report EIS on my tax return?

You will receive an EIS3 certificate for each investment. You can claim relief via your self-assessment or by asking HMRC to adjust your PAYE code.

Ready to build your tax-efficient portfolio?

Our Access EIS Fund uses a data-driven model to co-invest with the UK’s best-performing angel investors.

View current investment opportunities →

HMRC Helpsheet HS341: Official technical guide for claiming EIS income tax relief.

HMRC Helpsheet HS393: Official guidance for claiming SEIS income tax and capital gains tax reliefs.

HMRC Venture Capital Schemes Manual: The comprehensive internal manual used by HMRC to administer venture capital schemes.

Please note: our office hours are weekdays, 9.30am - 5.30pm.