Don't invest unless you're prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 mins to learn more.

The UK startup funding landscape has undergone significant changes over the past decade, shaped by monetary policy, inflation, and broader economic conditions. A detailed analysis of both the overall venture capital market and the Enterprise Investment Scheme (EIS) reveals fascinating insights into how different segments of the startup funding ecosystem respond to economic pressures.

The overall UK venture capital market: the influence of interest rates

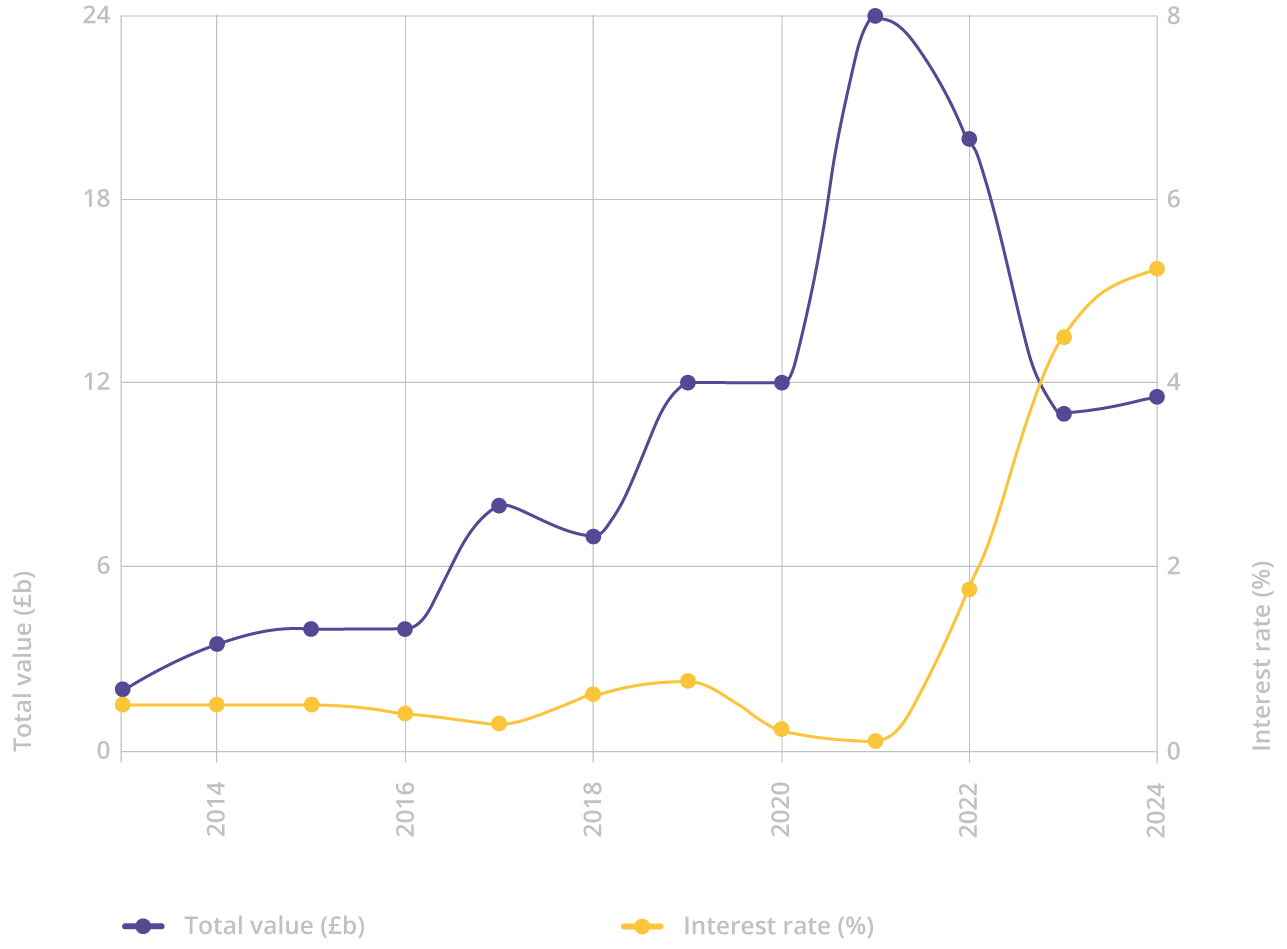

Total invested capital in venture capital deals compared to Bank of England interest rates

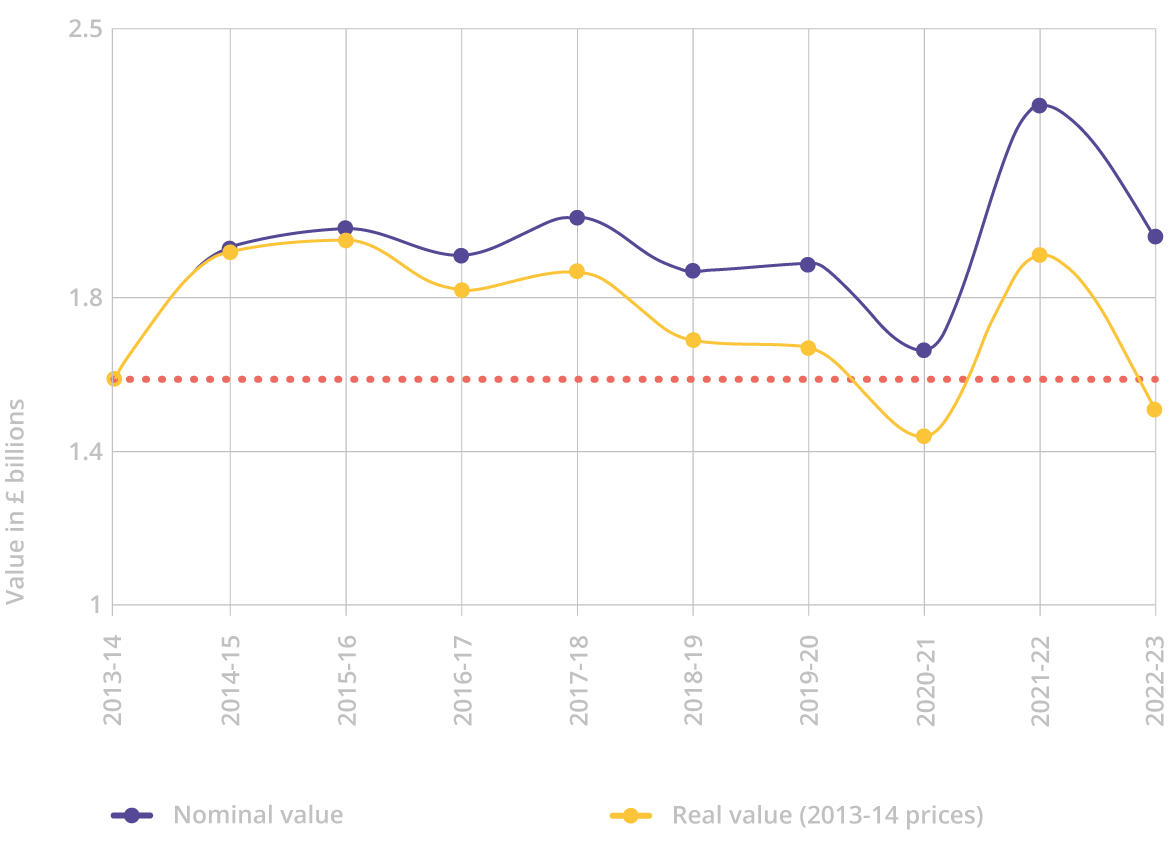

The overall UK venture capital market showed remarkable changes between 2013 and 2024. From a modest £2 billion in 2013, funding surged to a peak of £24 billion in 2021 before retreating to projected levels of £11.5 billion in 2024. You can see this compared to the average Bank of England base rates for interest, which underwent a surge in recent years as total investment dropped, and so there is a partial correlation. That is not to say there is causation but we can definitely theorise how the two could be interacting and what the mechanism would be. Importantly, these headline figures are heavily influenced by late-stage deals, which often dwarf early-stage investments in size. These rounds include large venture capital firms which have particular sensitivities to the broader capital flows and their LPs seeking yield. What this means is that when interest rates are low, large amounts of capital look for places where it can still get good returns. It does not benefit from sitting in cash or bonds, and so venture capital receives attention. However when interest rates increase, these large capital players can gain more from bonds and other safer investments. Moreover, there is increased risk that the startups will struggle to perform in a high interest rate, low spending environment. The prolonged period of near-zero interest rates fundamentally altered investor behavior. With traditional fixed-income investments offering minimal returns, institutional investors, pension funds and wealth managers were compelled to seek yield in alternative assets. Venture capital, with its potential for outsized returns, became an increasingly attractive destination for this capital. This "search for yield" phenomenon helped drive the market over a long period. However, the relationship between interest rates and venture funding isn't immediate; it involves a lag effect. Venture capital firms typically raise funds that are deployed over several years, meaning that even as interest rates began to rise sharply from 2022 onwards, previously committed capital continued to flow into the market. I suspect that the full impact of higher rates often takes 12-24 months to materialise as it primarily affects new fund formation and LP commitment decisions rather than immediate deployment. The dramatic spike in activity during 2021 requires specific attention to understand the current market context. Two key factors drove this unprecedented surge: 1. COVID-19 deal backlog: Many companies delayed their funding rounds during the uncertainty of 2020, creating a pipeline of delayed deals that were executed in 2021 as market confidence returned. 2. Government stimulus impact: The extensive financial programs implemented by governments worldwide in response to COVID-19 had an effect similar to quantitative easing, significantly increasing the flow of capital in the market. This abundance of liquidity, combined with low interest rates, drove investors toward high-growth opportunities in the technology sector. As we move into 2024-25, with interest rates nearly 5%, the market is adapting to a new reality where investors can achieve attractive returns through safer instruments. However, it is also likely that this cyclical factor could be counterbalanced by a powerful trend: the AI revolution. Much like the internet boom of the early 2000s, transformative technologies can create their own investment momentum, even in a high interest rate environment. We're seeing this particularly in AI-focused startups, which continue to attract significant capital despite broader market headwinds. Consider that global investment in generative AI reached $24 billion in 2024 according to EY, with the UK receiving $3.8 billion AI investment in 2023. Looking back at 2024 the market remained flat as interest rates didn’t come down significantly. I don’t expect us to see big cuts to interest rates in 2025 and so I don’t think we will see a big change in the market. However, the exception to this could be the already mentioned AI factor. If the UK can generate a wave of AI startups that are globally competitive, then they will quickly close mega rounds, and the topline figure of investment will expand once again. ## The EIS market: proven to invest in unicorns, yet declining in real terms The EIS market presents an interesting contrast to the broader venture capital landscape. While nominal values have remained stable, ranging from £1.6 billion in 2013-14 to £2.0 billion in 2022-23, with a peak of £2.3 billion in 2021-22, the inflation-adjusted figures tell a more nuanced story. Note that we are talking here about total EIS values claimed from investment, as reported by HMRC. So it includes all EIS round stages (although EIS is typically at an earlier stage) and all types of EIS investors. [

](/access-eis) *Total value of HMRC EIS claims (based on UK funding rounds)* So what is going on here? First of all we see a similar spike in 2021/22, and my theory is that this was EIS investors taking up their pre-emption in the larger deals happening in the market. Otherwise though, why is there a divergence between the overall market and the EIS market? **Market participants and stage sensitivity**: The broader VC market is heavily influenced by global institutional investors and their ability to deploy large amounts of capital. These investors are more responsive to interest rates and macro conditions. In contrast, EIS investments are smaller in size and typically come from UK high-net-worth individuals, whose investment decisions are influenced by personal wealth, tax considerations, and risk appetite. **Impact of inflation**: The real-terms decline in EIS investment values suggests that high-net-worth individuals' appetite or ability to maintain investment levels hasn't kept pace with inflation. This could reflect broader pressures on personal wealth, including stagnant real wage growth. Unfortunately I think this chart reflects tougher investment conditions for UK investors – either there hasn’t been an increase in their own personal wealth, or they are viewing the EIS market as too risky for the returns they’ve seen. Or it could be both. Note that this chart is not actual returns, but simply the absolute investment amounts. As we are a venture capital investor you might say we have a conflict of interest in claiming that it is still a good market for returns. So I would point to [Beauhurst’s figures](https://www.beauhurst.com/research/eis-30th-anniversary) that EIS has played a crucial role in funding 20 unicorns – private companies valued at over £1bn. Even more impressively, of the 43 active unicorns in the UK, 46.5% have benefited from EIS-backed funding. This remarkable statistic underscores the scheme's effectiveness in identifying and supporting high-potential companies at their earliest stages. However, despite the lack of real growth in the total investment, it also paints a picture of stability when compared to the more volatile overall market. One could argue that the dependability of nominal investment levels, despite significant economic headwinds, demonstrates the enduring appeal of early-stage investment opportunities and the effectiveness of the EIS scheme in channeling private capital to early stage companies. This helps to create a constant flow of startups which can capitalise when the late stage market does turn. ## Looking Ahead The outlook for 2025 presents both challenges and opportunities. While sustained high interest rates may continue to affect overall venture capital availability, sector-specific opportunities, particularly in AI, deep tech and green investments, could drive significant activity. The EIS market's structural advantages and focus on early-stage opportunities position it well to continue supporting the next generation of innovative companies. For the EIS market, the challenge will be to reverse the real-terms decline in investment values. This may require either a combination of lower inflation, higher real wage growth among potential investors, or enhanced incentives to maintain the scheme's effectiveness in channeling capital to early-stage businesses. As we move forward, understanding these distinct market dynamics will be crucial for both investors and entrepreneurs. The data suggests that while the overall venture market may continue to experience significant swings based on macro conditions, the EIS market's stability provides a more reliable foundation for early-stage funding in the UK ecosystem. ### The Carbon13 SEIS Fund Our latest investment opportunity is an SEIS fund focused on returns with purpose, building and backing early-stage businesses addressing Earth’s vital life support systems.

This fund, Carbon13's 7th SEIS fund portfolio, will invest in pre-seed companies that are expected to be eligible for SEIS, and enable investors to claim a suite of tax reliefs such as 50% income tax relief on up to £200,000 invested, and 50% exemption from capital gains that arise in the same year. Tax reliefs are subject to status and change. Click the button below to view the fund and make an investment. View the Carbon13 SEIS Fund ### The Access EIS Fund Our fund co-invests with proven angel investors to build large portfolios of hand-picked companies for our investors. It’s a high risk investment, and we can’t guarantee that every startup will be a unicorn, but we’re confident that our approach is the smartest on the market. Even better, we can show you the data to prove it. If you’re interested and would like to find out the benefits of investing towards the start of the tax year, you can call us on 01223 478 558 and we'll be happy to answer any questions you might have. Or, if you're ready to get started, click the button below: View the Access EIS Fund